Chubb's Climate Insurance Wars Have a Price: Ask Mexico

Six years of shareholder activism over Chubb's fossil fuel underwriting is now in federal court. The costs will be paid somewhere beyond the U.S., like Mexico.

On March 3rd, 2026, I woke up to the news that a few blocks from home in Washington, D.C., a San Francisco nonprofit had filed a complaint in federal court against Chubb Limited, one of the world’s largest insurers. The nonprofit, As You Sow, and Chubb have been embroiled in a never ending boardroom and legal battle since 2019 that may end up deciding whether climate change activists can exert indirect influence over climate policy in the Global North without political control earned at the voting poll. This strategy, however, may end up passing on the cost of Green Capitalism to the Global South in the process.

The relevance of this particular lawsuit is embedded in the nature of the ask, tucked behind the legal jargon. As You Sow argued that Chubb blocked a shareholder proposal containing one single demand: that Chubb commission a report to assess whether it is viable to “pursue compensation” from “responsible third parties,” to offset the cost of climate-related losses. In other words: As You Sow wants Chubb to sue the oil and gas industry worldwide.

At scale, this may produce deep, even crippling consequences for the petroleum business. The effects, however, would not be contained to the target industry alone. Cripple the fossil fuel industry at a global scale and you get a spillover effect extending to all the other industries highly dependent on it, including the logistics, infrastructure, transportation, and agricultural sectors. This is so because there is no substitute for fossil fuels today at scale. No matter what activism says, physics says otherwise, unfortunately.

But why Chubb?

Chubb is a company with global presence, with gross premiums revenues of $62 billion, and asset values of $272 billion. If Chubb were a country, its GDP would be larger than Iceland’s and its balance sheet would be the size of its entire banking system. Their reach and their pockets are deep. Then, there’s also what they do for a living.

Chubb’s core business by volume and revenue, its property and casualty (P&C) line, registered a $31.29 billion in net premiums earned (NPE) in 2019 and $53 billion NPE in 2025. P&C risk underwriting is what pays for your smashed phone, or your busted kitchen after you torched it cooking farmed salmon. This is Personal P&C. However, P&C is also what pays for a blown up oil refinery in the Gulf after an accident, it is what secures project finance or lending for a state-owned oil company like Mexican PEMEX to drill, and it is also what pays for cold storage for agricultural produce waiting to be carted north to the United States. This is Commercial P&C, and Chubb’s Commercial P&C is about 38% of its total NPE in North America alone.

Chubb, as it turns out, is virtually present in every aspect of the mechanisms that control our daily lives, like our communications, our transportation, our electricity, the packages we order on Amazon or Shein, and the food we put on our table. Through its clients, Chubb underwrites risk, insures and invests with a depth that no other industry has the power to replicate. Thus, Insurance is king.

To Kill an Industry, First Kill Its Insurance

Every major industry in the Global North faces moral and material pressures to adopt more climate-friendly policies and corporate strategies. Aeronautics could develop more fuel-efficient turbines; Mining could deal more competently with waste and tailings. For those industries and many more, it is relatively easy to point to the pressure point and target it. However, insurance is different insofar as the industry itself is not where the target of climate activism is, but rather the infrastructure that sustains it. That is, a coal company can be protested and divested from, and it will still operate as long as it can finance and insure its assets.

This defeats the purpose of climate activism. Thus, activists realized that if they cannot eradicate an industry directly, they must remove the preconditions for its existence. Insurance is one of three such preconditions, alongside with banking and project finance. A business cannot build, operate, or finance an industrial asset without insurance in any modern economy. There’s no escaping this basic financial tenet.

This makes insurance the master key to all other target industries. A bank can be pressured to stop lending to fossil fuels, but the bank can be replaced by another bank, including non-Western ones beyond the activist’s reach. However, when Chubb underwrites a refinery or a port terminal, it does not carry that risk alone. Instead, Chubb re-distributes that risk across a network of global reinsurers to share the burden if the assets are lost. That industry network is finite, and it faces the same activist pressure simultaneously. There is no replacement for this industry. Thus, if activists pressure an insurer of Chubb’s caliber to stop guaranteeing certain activities or to operate under certain criteria, the replacement problem becomes systemically impairing for the uninsured.

Insurance, also, is special because of its access to information. On paper, an insurer knows more about a client’s operations, risk profile, and exposure than almost any other counterparty. Activists understand that embedding greenhouse gas (GHG) emissions criteria into underwriting decisions means embedding climate policy into the most intimate financial relationship a company has, where the insurer can demand disclosures, set behavioral conditions, and price non-compliance directly. No other financial intermediary has that operational visibility.

Enter the climate insurance wars.

An activist call to arms: Chubb stops underwriting coal in 2019

The standoff between the activist shareholders and the insurer didn’t just suddenly come to a head this March. It all started with seemingly good news in 2019, when Chubb announced, of its own accord, that the company would stop underwriting risk for coal-related activities and investments. This was, in all honesty, an important step forward in fighting climate change.

Chubb committed to stop insuring new risks for companies that generate more than 30% of revenues from thermal coal mining and to phase out existing coverage by 2022. At the time, this was framed by Chubb’s CEO, Evan Greenberg, in the spirit of environmental stewardship. Across the boardroom, however, an activist shareholder coalition read the move as a tactical opening and an invitation to escalate. Chubb, in that moment, did not realize that a particular logic was being embedded in the activist rationale for the company: a concession, instead of a settlement, was actually both a sign of weakness from Chubb and a beachhead for the activists’ climate goals.

The first coordinated action happened in 2022, when Green Century, one of the activists in the coalition, filed a resolution requesting Chubb to adopt policies to stop underwriting new fossil fuel extraction, in line with the IEA’s Net Zero Emissions by 2050 Scenario. As You Sow, separately, filed a proposal requesting Chubb to issue a report on whether and how it intended to measure, disclose, and reduce GHG emissions from its underwriting. The Board recommended against both proposals. Green Century’s proposal was voted down, but As You Sow’s passed, after garnering more than a 72% support. This is how the highly controversial Scope 3 protocol entered the world of Chubb Limited.

This was a pivotal moment and the height of institutional support for the coalition’s goals. The kind of support that As You Sow’s proposal received was not a mere protest vote. Nearly three quarters of institutional shareholders voted yes, including the New York State Common Retirement Fund, a nearly $298 billion investor behemoth with political clout that represents a key U.S. constituency of over 1.2 million New Yorkers.

That year of 2022, I spent my spring break at the U.S.-Mexico border in Laredo, Texas, conducting interviews in Spanish with destitute immigrants turning up at the border. To get there, I’d driven south from San Antonio. The highways of Texas stemming from the border were an endless stream of north-bound trucks carrying products to the interior of the United States. The large majority of these fabulous fleets of diesel sponges were carrying agricultural products. I was amazed at the sheer scale of the logistics keeping the United States fed, and got overwhelmed at the thought of the operating costs of these supply chains. Then and there, and for the longest time, I did not realize that each truck, the owners of the cargo, the people loading or unloading goods, the fuel producer, all had two things in common: they depended on the petroleum industry, and they all needed insurance. Knock down a single one of these delicate pieces, and the system collapses like a domino chain.

By 2023, Green Century tried again to phase out all fossil fuel underwriting. Chubb suppressed the initiative by taking the matter to the U.S. Securities and Exchange Commission (SEC.) The SEC found for Chubb, saying that in their view, the proposal micromanaged the company. Chubb won the procedural fight, then immediately announced an oil and gas underwriting restriction in protected areas, surrendering the point. As You Sow, meanwhile, re-filed and lost its Scope 3 proposal. This time support collapsed to 28.93%.

The signs were clear that activist pressure was not relenting. The government also got involved in the summer of 2023. The U.S. Senate Budget Committee opened an investigation into the underwriting practices of major insurers operating in the United States, dragging the controversy to the public eye. In 2024 Green Century and As You Sow co-filed for Scope 3 one more time, but by then the mood on the topic had soured across the shareholder crowd, and support collapses again to 28.3%.

Scope 3: When the Math won’t cooperate and nobody backs down

It should be said that the proposals based off Scope 3 disclosures were not a vague gesture toward greener values. This was a specific technical demand made to Chubb to implement: collect GHG emissions data from every entity Chubb insures, across their entire value chain, processed against international reporting standards, and embed those emissions profiles into underwriting decisions.

Chubb’s Board correctly understood that this was methodologically impossible, including from a scientific point of view.

In their proposals, the activist coalition repeatedly asked for a highly advanced, technically complex combination of often unavailable data disclosures by third parties in the value chain of the underwritten activities, as well as for reporting practices that remain unstandardized, and resource allocation efforts that may not be reasonable to expect, even in the context of a large company like Chubb, which commands a great deal of human and financial capital. Indeed, Scope 3 data collection would require disclosures by entities throughout an insured client’s entire supply chain, who are generally private companies in multiple international jurisdictions with no legal obligation to report anything.

If a company is based in and operates from select areas of the Global North, on a relatively closed-loop supply chain, with relatively known (and a small amount of) partners who share the same regulatory, fiscal and incentives regime, then Scope 3 may not seem such high-bar standard to comply with. However, when you operate at a global level, and your business covers virtually every aspect of commercial (and non-commercial) activity under the sun, the task of complying with Scope 3 becomes not just Herculean, but simply unfit for the purpose.

In the case of Chubb, their legacy business model is different from that of a research institution, which is what the company would have had to turn into in practice, to satisfy the standards of Scope 3. That is, Chubb’s subject matter expertise lies in assessing risk on a case-by-case basis, not on a global scale as the GHG disclosures system requires.

At least until the end of 2024, the proxy campaigns for Scope 3 persisted, but the votes in favor continued to be low, even as Chubb repeatedly made important concessions. The insistence on the point, however, wore down the patience of the institutional shareholders, and their support for the activist coalition declined considerably.

Mexico and the cost dilemma of the humble tortilla

At the very end of 2024, I am in Mexico City for work. I am in a high-rise office in La Reforma, surrounded by U.S. State Department officials, taking notes like a maniac on security cooperation programs between the Mexican and U.S. governments. I can see the Angel de la Independencia Monument from the window, barely a block away, and the Popocatépl volcano smoking away in the distance. It’s so beautiful and perfect.

Yet, when I come downstairs during lunch, I realize that prices are higher than they were six months earlier, when I last visited. It is not lost to me this time that a lot more people are buying their food from street stalls than they are sitting in restaurants. Masses of white-collar workers are huddling around the budget-friendly stalls.

I spent a week having lunch around the office, and befriending the stall vendors. In snippets, I learned from them that there was a drought that year, and the crops were not that plentiful, so the price crept up little by little. Mexico’s government had also cut off subsidies for the country’s major corn producers after a reform in recent years. This forced Mexico to import large quantities of corn, including from the United States.

If the corn comes from farther away, the corn tortilla’s price experiences upward pressure. The entire supply chain runs on the diesel that powers the trucks, the trains, the ships, the cranes at the ports, and the corn mills. In the 2018-2024 period, the cost of tortillas steadily rose more than half, from MX$14.33/kg to more than MX$22.0/kg. Thus, diesel is not only the lifeline of the Mexican tortilla, but also its price floor. This is not to say that climate activism caused a tortilla price spike in retrospect. Rather, it means that activism is certainly not factoring in any of these costs when trying to decide future climate policy, with global implications, through boardroom battles and lawfare in U.S. courts.

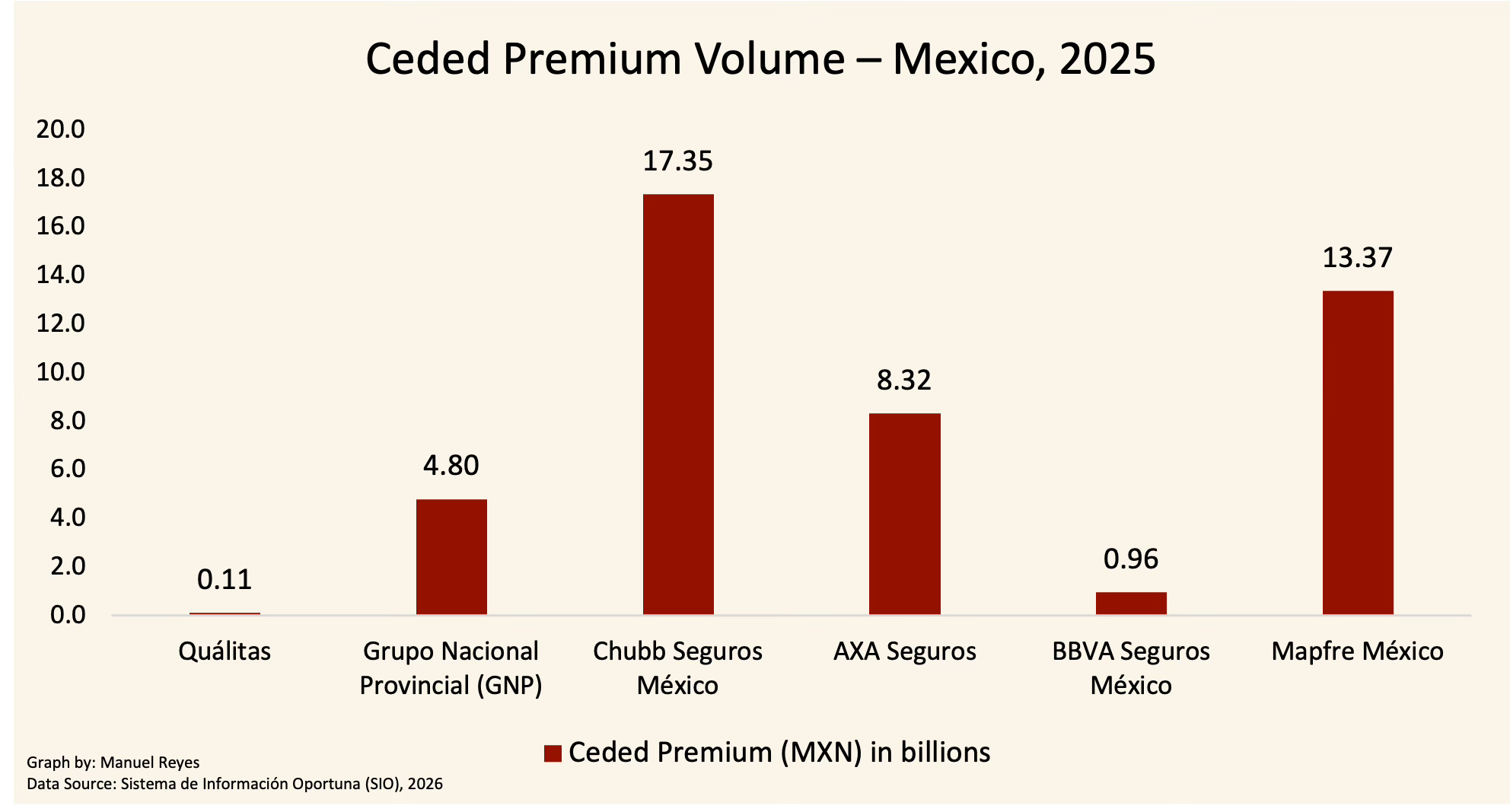

Chubb is the third largest property and casualty insurer in Mexico by total premium volume, writing MXN 28.2 billion annually. Within that book, the industrial lines matter most. In General & Commercial Liability, covering operational risk for refineries, gas pipelines, and petrochemical plants, Chubb writes MXN 2.04 billion annually. In Marine & Transportation, covering logistics chains moving fuel, produce, and manufactured goods across the country, MXN 1.79 billion. In Fire & Industrial risk, covering fixed industrial installations against explosion and damage, MXN 1.49 billion. And in Catastrophic Risk, covering tail risk on large-scale infrastructure, MXN 1.68 billion. This is the insurance backbone of Mexico’s fossil fuel-dependent industrial economy, and the coverage that no domestic Mexican insurer has the reinsurance architecture to replace.

Thus, beyond incremental curtails of fossil-fuel underwriting, if Chubb is also eventually steered into suing the fossil fuel industry, then the consequences may extend well beyond the target. Activism would not simply be effecting justice for homeowners on the coastline of New York or on the wildfire-prone hills of California, they would also be creating, slowly, the conditions for structural food shortages and political unrest in the Global South. Mexico is but a sample drop in a sea of countries dependent on insurance to finance their agricultural, infrastructure and logistical operations.

The cost transmission mechanism of climate insurance, and the lawsuit in D.C.

In Mexico, what makes Chubb’s role structurally distinct from a regular market participant is not even its balance sheet exposure. Rather, what’s important is its position as the point of entry into the global reinsurance network. Chubb is the biggest cedent in Mexico by total premium volume, 30% ahead of its closest competitor, Mapfre. What’s more, if Chubb were to exit the country and Grupo Nacional Provincial (GNP)—Mexico’s second largest P&C insurer—tried to absorb its book, GNP would need to multiply its entire reinsurance cession by a factor of four.

When Chubb underwrites a PEMEX offshore project or a cold-storage logistics hub in Monterrey, it redistributes about 61.5 cents of every peso of premium into a chain of international reinsurers who absorb the tail risk. Again, re-distribution is what makes large-scale industrial activity insurable in the first place. Restricting Chubb’s legacy business model will not simply remove one insurer from the Mexican market, but rather impair the access point to the entire chain. Without it, the risk becomes uninsurable at a cost, and therefore unfinanceable.

In 2025, Green Century tried to get Scope 3 passed one last time. Support cratered to 13.9%. As You Sow took notice and moved on from Scope 3, understanding that the way to keep going was to sprint ahead. This is what led As You Sow to file the proposal that Chubb last tried to suppress, and that landed them in Court this March, after the SEC refused to intervene.

This lawsuit now sits astride the convergence of administrative law, securities regulation, and corporate governance, all at the same time. As You Sow is no longer asking for meticulous directives of Chubb’s day-to-day operations, like Scope 3 required. That would land them again in the trap of shareholder overreach. Instead, they are cleverly asking for a report that would force Chubb to evaluate its own corporate posture on climate liability, which could then be resolved by the routine mechanism of subrogation. There is a question of public policy.

A substantive issue of law is being presented as a procedural matter. It may be that As You Sow is using the threat of court as a dispositive tool, simply to make Chubb settle quickly by re-including the proposal in this year’s shareholders meeting. Chubb, on the other hand, may try to stall the case, unglamorously, until proxy season is over and the issue becomes moot, instead of trying its hand at litigation in a case so inscrutable.

Caution, market sense, and science should be the guiding principles of exerting influence over companies, not zealotry alone. The solutions to climate disasters are not solutions at all if a minuscule group of constituents in one corner of the world imposes top down policies through the conduit of a multinational corporation outside all democratic processes. Activism for climate change, however laudable, cannot turn into ideological capture of any or all institutions with a balance sheet. This is so, especially, if the costs—which are serious—are just being swept under the rug and sent elsewhere later.

To the South of the globe, the realities of life are still run by combustion engines and extractive economies. The Global South is already paying for climate change in drought years, in erratic harvests, in coastal erosion, in extreme heat oscillations. Indeed, the Global South also contributes to climate change, but it did not cause the original problem in any proportionate sense. Now, it may soon be asked to pay again, in higher logistics costs, in restricted access to project finance, in uninsurable infrastructure. The folks selling or buying tortillas in Mexico City may eventually absorb both bills, as a tax they did not vote for, imposed by people no one elected to hold office, neither in their country nor in the U.S.

What to read next:

_-_1.jpg?uselang=en#Licensing){kind=link}

See The Southern Trade on Google

Want The Southern Trade analysis at the top of your feed? You can tell Google to prioritize this source by clicking on the button below.

© 2026 Manuel Reyes, The Southern Trade Group™. All rights reserved. Content may not be reproduced without permission.