ST Monitor | May 2026 | Resources Realignment Under Political and Market Pressures in Latin America

Focus: Colombia’s Ecopetrol, Argentina’s Super RIGI, Guyana’s and Suriname’s Oil Industry

In this Edition | May 2026

Political decisions and market pressures in Latin America are reshaping control of resource extraction and allocation in several countries. These include governance failures, development priorities, and electoral transitions. This month’s edition covers four situations where reshaping of natural resources control, capital allocation, and revenue inflows are actively underway, at different stages of resolution.

In Colombia, Ecopetrol’s governance crisis has reached an impasse under Petro, and incoming administrations face inherited damage that is unlikely to be corrected quickly, regardless of who wins the upcoming presidential elections. In Argentina, Milei’s Super RIGI arrives in Congress as a USD 1 billion greenfield investment with aggressive deregulation, and a provincial adhesion mechanism that may prove more decisive than the congressional vote. In Guyana and Suriname, oil revenue management at scale is increasingly becoming both countries’ priorities, with Suriname now securing the financing to follow Guyana’s playbook offshore.

The ST Monitor proprietary classification is applied to interpret specific developments across Latin America based on their phase of execution. Some plans remain at the level of (1) political signaling without an operational framework; others are (2) constrained within permission-based systems; and others are (3) fully operational and institutionalized. The cases chosen for this edition should be read through that lens:

Level 1 — Pre-policy (no executable framework exists)

Level 2 — Constrained execution (activity exists but is permission-bound)

Level 3 — Execution Phase (system is operational and institutionalized)

Colombia: Ecopetrol’s Governance Crisis Reaches Its Logical End

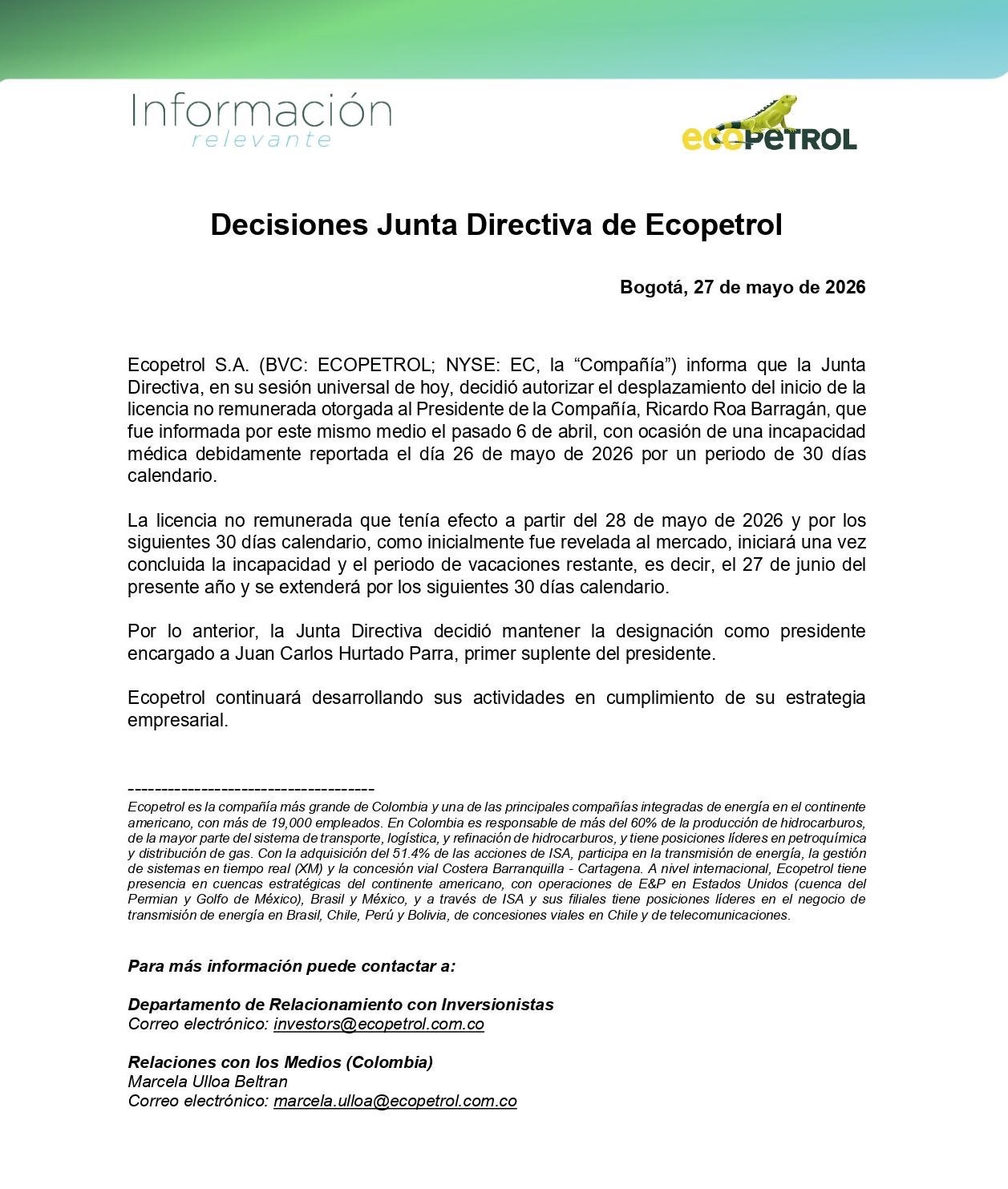

The Ecopetrol governance crisis has moved beyond board dysfunction into institutional paralysis right at the gates of a presidential election in Colombia. The institutional drift of the largest company in the country may have serious impacts on Colombia’s fiscal health, if the situation is not corrected by the next administration.

On May 26, Ecopetrol’s CEO Ricardo Roa filed a medical leave notice with the company’s board, which approved a 30-day extension of his absence. Combined with existing vacation and unpaid leave already authorized, Roa will not return to the presidency of the SOE until July 27, 2026. The date falls within two weeks before Petro’s government ends. Thus, the executive that Petro installed as president of Colombia’s most important company, and whose conflicts of interest have been the subject of two criminal indictments by the country’s Attorney General, may return to his post barely a moment before the entire political architecture that protected him dissolves.

Additionally, on May 12, Juan Gonzalo Castaño resigned from Ecopetrol’s board. Castaño had, over time, taken positions that distanced him from Petro on two sensitive questions: he voted against Ecopetrol exiting the Permian Basin position, and he was part of the board majority that approved Roa’s temporary removal. His resignation may not be a voluntary departure after all, and rather just another interference by the Petro administration, enforcing board loyalty to the executive.

The Colombian elections will be decided on May 31, and a run-off may ensue on June 21 if needed. It is upon the winner to decide how to stabilize and reform the company they inherit. Ecopetrol is listed in the New York Stock Exchange (NYSE), and therefore exposed to SEC disclosures, DOJ and FCPA jurisdiction, among others. To reverse course, the new Colombian executive may need to address the exploration moratorium (including a fracking ban), the circumstances of the Crown Rock project exit, or the previous en-masse executive departures of the Petro era.

The candidates for the Colombian Presidency represent differing levels of engagement with the petroleum industry. Leading the polls is Senator Iván Cepeda, a committed left-leaning ideologue, often described as much more intransigent than Petro in his support for an assertive government or on his position against hydrocarbons. Likewise, Cepeda is expected to continue Petro’s policy of “Paz Total” (Total Peace), where the insurgent groups within Colombia are no longer considered to be motivated by ideology, only profit and criminal interests. Criminal activity and violence by insurgent groups has surged under the Petro administration.

If Paz Total remains the position of a prospective Cepeda administration, then onshore operations in Colombia’s E&P activities will remain subject to a risk premium for longer. This is so because if the State no longer sees insurgent groups as motivated by ideology and still decides to engage in negotiations with them, then the government is effectively renouncing its role as guarantor of security over its own territory. That is, the State is recognizing criminal groups as legitimate interlocutors in an official dialogue over the groups’ rights. This is not to say that an enforcement approach should be prescribed instead, just that Paz Total elevates the status of what should now be considered common criminals, if such insurgent groups no longer harbor political aspirations.

Taken together, Ecopetrol remains burdened by severe weaknesses in governance. Furthermore, it is unlikely that a change in Colombia’s presidency will mean a short-term solution to the company’s crisis or to its mid-term outlook. This is especially so under a future Cepeda Administration, who may be hostile toward the petroleum industry and lenient towards criminal activity within Colombian territory. Finally, it is also not clear that trailing candidates Paloma Valencia or Abelardo de la Espriella—although friendlier toward hydrocarbons—have answers to the company’s woes or the country’s political pressures.

Overall, Ecopetrol faces internal challenges and political problems that may continue to affect the company’s performance, and in a worse case scenario, even threaten institutional continuity.

Status: Level 2 — Constrained execution

Argentina: The Super RIGI Arrives in Congress, Milei Flexes Executive Muscle

Argentina’s executive submitted the Régimen de Incentivo para Grandes Inversiones en Nuevas Industrias (Super RIGI) to the Chamber of Deputies on May 26. The new regime sets a USD 1 billion minimum investment threshold, a 15% corporate tax rate, full import and export duty exemptions, unlimited loss carryforwards, and a 30-year tax, customs, and FX stabilization guarantee locked in as an acquired property right from the moment of adhesion.

The regime targets new industries that do not currently exist in Argentina or are in the experimental stage. Only greenfield projects will be considered. The original RIGI, enacted via Ley Bases in 2024, is explicitly excluded. The executive has singled out AI, semiconductors, advanced biotechnology, and digital infrastructure as strategic targets.

The passage of the draft law is likely, but not guaranteed. The Milei government does not currently hold a simple majority in either chamber of Congress. Thus, the critical path may run through governors, not legislators per se. Provinces must adhere individually, and governors who adhere will get projects while those who do not get nothing. To this effect, it is important to note that the draft law allows early adhesion by the provinces, independent of the voting process in Congress.

There is the carrot and stick mechanism by the Milei administration: Adhere early and get federal backing for local development; reject adherence and risk neglect from the executive. This binary choice embedded in the logic of the draft law may well come to define the political process ensuing submission. That is, provincial appetite for the perks of the draft law may tip the balance for or against the law, in lieu of strong Congressional support. Adherence from Buenos Aires (CABA) or Córdoba, for example, would be early indicators of viability.

Consequently, the Super RIGI’s deregulatory push is setting up a political fight in Argentina, not just over investment rules, but also over where capital will actually land in the country. The Milei administration is already negotiating directly with governors, pitching the regime as a provincial development tool to either pressure Congress to sign off on it or bypass the legislature altogether by securing enough provincial adherence before passage.

In that sense, the Super RIGI may end up reading less like an investment regime and more like a map of winners and losers across Argentina. Ironically, the most libertarian president in Argentina’s recent memory is arguably availing himself of the centralizing powers of federalism to bind local and national autonomy to his political agenda. That is, Milei is seeking to override congressional powers and recalcitrant provinces by forcing them to opt into his plan or be left out completely of major economic investments in the future. The draft law is, in practice, a maximalist political stance, despite its veneer of congressional procedure.

Whether the law passes with amendments or not, its spirit will remain the same: aggressive deregulation of the role of government as an economic and administrative actor, and gradual relaxation of capital controls.

I published a special report with full primary source legal analysis on May 27. All components regarding the draft law, including compliance implications for foreign investors, eligibility requirements, tax regime, dispute resolution mechanisms, and FX and capital controls are discussed in detail.

Status: Level 1 — Pre-policy (pending congressional approval and provincial adhesion)

Guyana’s Oil Output in Crescendo, Suriname Eager to Follow

Guyana

Guyana’s government reported its oil lift revenue for Q1 2026. The numbers were published in early April by the Natural Resource Fund (NRF): $761M. That tallies to well over three-quarters of a billion dollars in 90 days, in a country smaller than Idaho, with a population of barely one million people.

For a nation with historically low levels of institutional organization, the present-day Guyanese government’s ability to capture and manage oil revenue in an organized and relatively transparent manner is no small feat.

From an institutional standpoint, Guyana appears to be rapidly transitioning away from a small, low-capacity state with a commodity-based economy, chronic political fragmentation, and a thin administrative apparatus into a much more organized, rent-absorbing petrostate in rapid formation.

Before the Stabroek discovery in the 2010s, Guyana struggled with a minimal industrial base, economic activity oriented mostly toward sugar, rice, and gold mining, and contentious politics. Now, the oil riches guarantee revenue, but pose the question of whether the government can develop the absorption capacity for hydrocarbon rents in the long term, while politics remain fractured along ethnic lines and special interest groups.

The monthly inflows report from the NRF confirm the upward trend. The Stabroek Block brought the Natural Resource Fund (NRF) balance above USD 4.1 billion for the first time by early May, as a combination of oil revenue, royalties, bonuses, and interest income. Guyana has gone from a $4.28 billion GDP in 2015 (when Exxon first announced the Liza-1 discovery) to $24.66 billion in 2024. Its debt-to-GDP ratio (29.2%) and inflation levels (4.1%) are considered manageable and well within what the oil rents can absorb.

Overall, in its first decade since the oil discoveries, Guyana seems well-adjusted to the newfound oil bonanza, including by both fostering oil production growth and putting in place a basic fiscal mechanism to manage the revenue inflows. The country produced 830,000 bpd in 2025 and expects to expand further this year to 840,000 bpd.

Status: Level 3 – Execution Phase

Suriname

Staatsolie, Suriname’s state-owned oil company (SOE), raised $516M through their 2025-2033 bond scheme and also secured a $1.6 billion syndicated loan from a “consortium of 18 banks and financial institutions.” This development has not received much coverage from traditional outlets, with few exceptions.

The news appeared in Staatsolie’s 2025 Annual Report, released in mid-May. Paramaribo appears to have carefully studied its neighbor’s success and wants to reproduce Georgetown’s playbook in the offshore upstream.

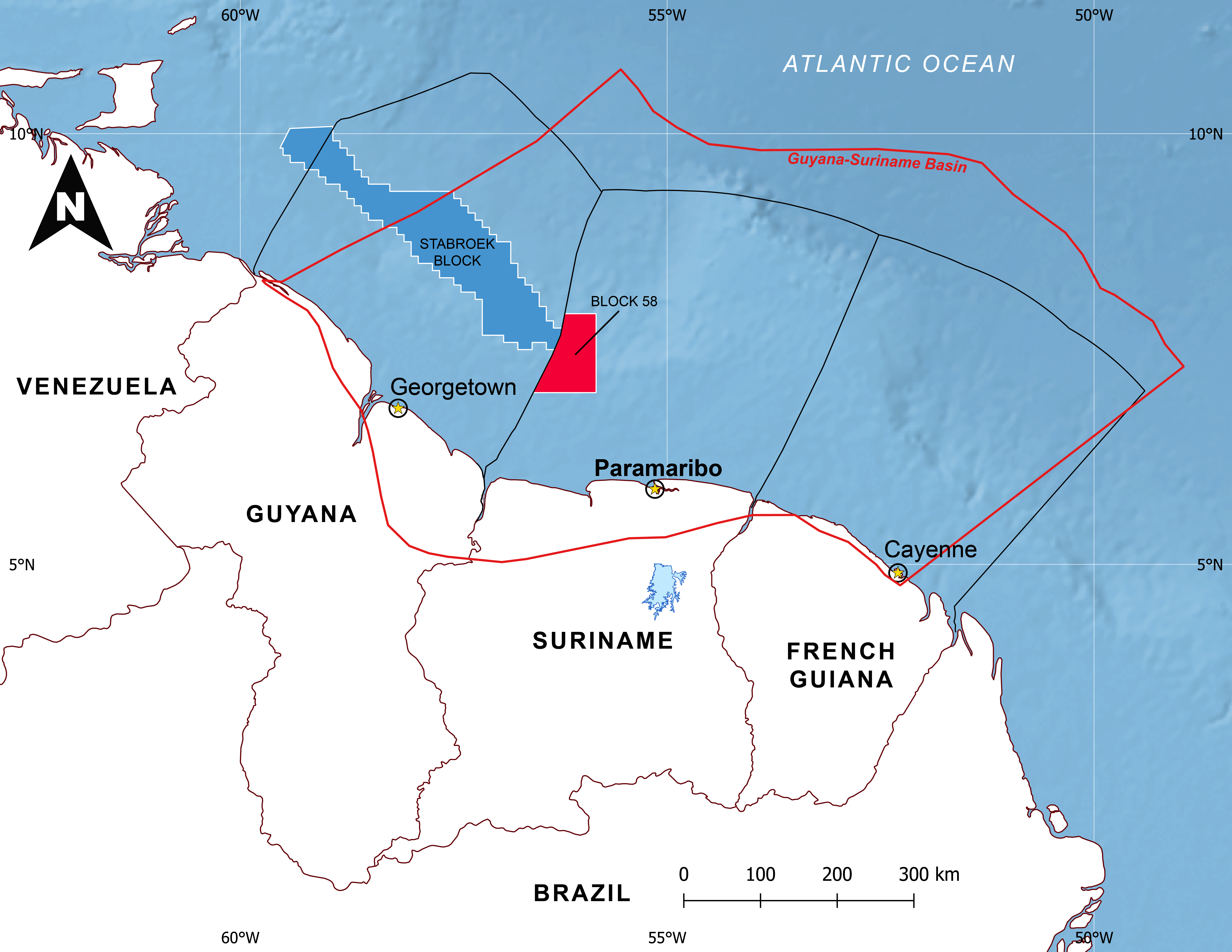

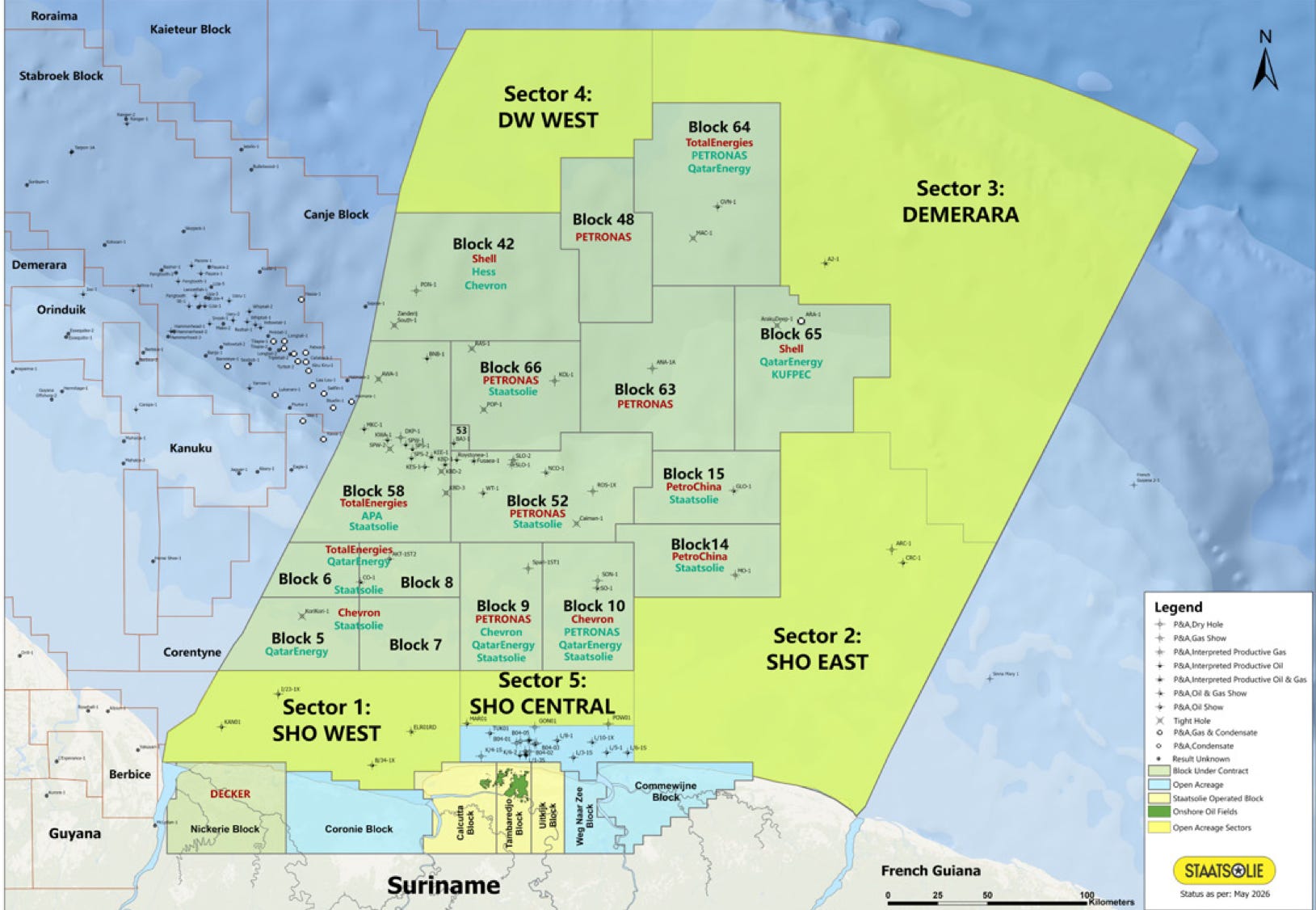

Staatsolie’s institutional capacities are neither underdeveloped nor unexperienced. This company has been extracting conventional oil in Suriname for decades. In 2025 Staatsolie produced a modest 17,400 bpd onshore, which entails a certain baseline of technical development and a skilled workforce in place. The SOE has associated itself with a number of international oil companies (IOCs) for E&P activities offshore, especially in the Gran Morgu project (Block 58), a deepwater play that could yield up to 220,000 bpd at peak production, once online. French Total Energies is the project’s main operator and Staatsolie reserved a 20% stake option for itself. Drilling is expected to start in Q4 2026.

However, Suriname faces several institutional challenges that could hinder its ability to harness and manage future oil riches—including patronage networks inside the government, driven by ethnic-based clientelism. Suriname’s bureaucratic structure is inefficient and bloated and suffers from low-credibility among its citizenry. Likewise, legacies from the Bouterse era remain entrenched administrative practices, including the government’s outsized role as an economic actor and distrust of the private sector through regulatory barriers to growth.

Overall, Suriname has the political will to expand the petroleum industry and become a net oil & gas exporting nation in the medium term. Nevertheless, although plans to expand offshore E&P activities are in place, Suriname’s weak regulatory environment and clientelism may prevent the country from realizing its productive capacities in the immediate future.

Status: Level 2 — Constrained execution

Other Relevant News to Observe:

Venezuela | Debt Restructuring Announcements: The Venezuelan government announced plans to restructure its debt, but this remains at the preparatory stage only, as full negotiations are still blocked by OFAC sanctions.

Watch for: Any further OFAC licenses that would allow actual creditor engagement versus continued legal posturing. It is clear by now that there is a political will in Washington to rehabilitate Caracas into the global financial system, but progress is not guaranteed and each action by the Trump administration on Venezuela should be carefully analyzed before taking it at face value.

Brazil | Oil Royalties Dispute at Supreme Court (STF): Brazil’s Supreme Court resumed hearings on the constitutionality of the 2012 oil royalties’ distribution law, a case with major fiscal implications for producing vs. non-producing states.

Watch for: a decision favoring non-producing states. Revenue certainty for producing states is the main factor for IOCs at the time of

investing. The 2012 royalties law gives producing states a larger share of pre-salt oil revenues. Producing states will lose substantial income if the STF rules in favor of greater redistribution to non-producing states. This may translate to higher local taxes or royalties demanded from operators to compensate for lost funds, and weaker local infrastructure investment (ports, roads, workforce training) that supports offshore operations.

Brazil | PPSA Delays and Scales 6th Oil Auction: Brazilian state-owned PPSA has postponed the 6th Pre-Salt oil auction from July to August 2026, citing the need for more stable market conditions. The agency is also considering increasing the volume on offer from 106 million barrels to 110–115 million barrels and may split the process into two separate auctions.

Watch for: Indications of what PPSA considers “more stable market conditions” and whether the delay leads to better terms, or on the contrary, if it signals growing caution by Brasília amid the Hormuz crisis effects on international reserves and whether Brazil may be planning to hedge for a supply crunch, particularly at a delicate fiscal and regulatory time ahead of elections.

If you liked today’s issue, forward it to anyone who should be reading it

🔗👇 Share this newsletter by clicking the icon below!

See The Southern Trade on Google

Want The Southern Trade analysis at the top of your feed? You can tell Google to prioritize this source by clicking on the button below.

© 2026 Manuel Reyes, The Southern Trade Group™. All rights reserved. Content may not be reproduced without permission.

.jpg?uselang=en#Licensing){kind=link}