Food Security with Chinese Characteristics, or How to Make Brazil Pay for Your Soy

From farmgate to port: How China captures value in Brazil’s soy supply chain without controlling land.

Key Takeaways:

A new neocolonial pattern is emerging in Brazil. China captures value in Brazilian agribusiness not through land grabs or coercion, but through controlling inputs, trade, and infrastructure, subsidizing its own food security while leaving Brazilian sovereignty formally intact.

Brazilian farmers experience margin compression under this model. Even though prices are market-driven, concentration of infrastructure and trade in Chinese hands shifts the competitive equilibrium, limiting the farmer’s own productivity gains.

China may influence price discovery. Controlling infrastructure and origination may allow Chinese SOEs to affect market timing and conditions, ensuring Brazilian soy costs less to deliver to China than competitors, even without directly setting prices.

Last year, passions stirred when the Brazilian government modified the original tender offer of a mega terminal in the Port of Santos.[1] The shipping industry and the political spheres were flustered, after Brazil’s Port Authority (ANTAQ) followed its own recommendation to sideline established port operators from the tender process.

Brazil almost surpassed the U.S. as an agricultural exporter in 2025. At $169.1 billion sold in agricommodities last year, Brazil’s rise as the next global breadbasket seems less a question of if and more a question of when.

The tender offer process keeps delaying, after Brazil’s auditing body (TCU), upheld ANTAQ’s decision. Last March, the U.S. Consul-general in Sao Paulo cautioned port executives against allowing China to clinch the concession of TECON 10, the mega terminal. The result of this battle may offer clues as to whether Brazil has a plan to capitalize on their agronomic progress, or if instead, they will revert back to being an agricultural neo-colony.

A global breadbasket in the making: Brazil’s ascent to the top of global agribusiness

In 1971, an obscure U.S. Department of Agriculture report noted that Brazil was an upstart agricultural nation, quickly rising through the ranks in export volumes. The main rationale behind it was that Brazil, like the U.S., could produce high-yield soybean crops, high in oil content, which would then go to the profitable crushing industry instead of table food alone.

At the time, only the United States and China produced more soybean than Brazil, respectively.

However, there were other powerful factors driving this agricultural development. The Brazilian government had an elaborate scheme of incentives and policies to wean itself off from food imports. These included R&D on seed strains, crop adaption to tropical areas in center-west Brazil, adopting floor prices for agricommodities, offering federal loans to farmers, compelling commercial banks to destine about 10% of their loans for agricultural production, and favoring the expansion of wheat crops. Wheat planting, specifically, reinforced another incentive scheme where Brazilian farmers entered a yearly, double-crop system of planting soybean immediately after harvesting the wheat.

Wheat, like corn, is a heavy feeder on nitrogen, so the soybean—a legume—was a perfect free nitrogen fertilizer and summer crop, following the winter wheat. The machinery for wheat crops, also, could be shared with the soybean crop, which in turn expanded mechanization, cooperatives, and storage capacity.

The report warned that Brazil’s soybean market was to be observed closely, as the South American nation could turn into a U.S. competitor, eventually.

This was over half a century ago—or 55 years, to be precise.

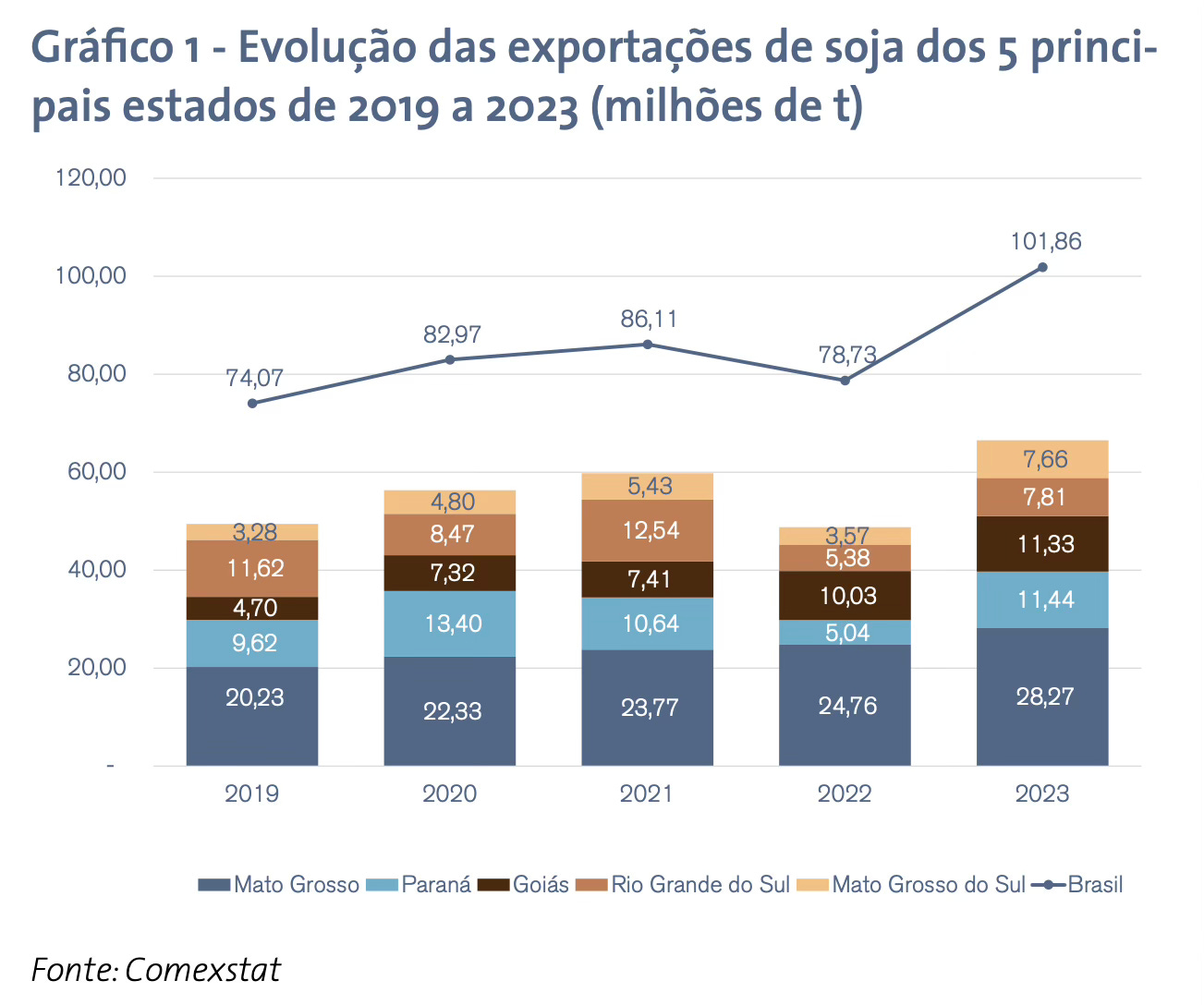

Today, Brazil dwarfs the rest of the world in soybean production. In 2025, Brazil produced over 166.1 million metric tons (MMT) of soybean, while the U.S. harvested 115.9 MMT, and China accounted for 20.91 MMT. The world combined yielded over 400 MMT.

Thus, Brazil is 41.5% of the global soybean market: They are the market.

As the world population continues to grow in the dozens of millions every year, food security is an increasing concern for governments around the world. Among the most concerned: The People’s Republic of China.

Connecting China’s social stability, the CCP, and the Brazilian soy market

China has a tough job when it comes to food. China is home to about one fifth of the world population, but it holds only some 9% of its arable land and 6% of its freshwater. This creates a food security bottleneck that could affect governance and the stability of Chinese Communist Party (CCP) rule in the country.

As a Marxist-Leninist institution, by design, the CCP partially draws legitimacy from material-abundance agendas. In other words, the CCP’s legitimacy hinges on delivering tangible economic and material benefits to the population, as its Soviet predecessor illustrated, in the negative.

China’s agricultural sector has modernized significantly, but the country is still technically inefficient, soil fertility is low, and corruption and disorganization still hinder crop output levels.

The General Secretary of the CCP, Xi Jinping, included food security in his Holistic National Security approach. However, his (public) concern with food can be traced back to 2013, during the annual Central Rural Work Conference. By Xi’s account, China should “[m]ake reasonable use of the international agricultural products market”, and “formulate international trade strategies for important agricultural products,” including by optimizing the “layout of import sources” through “stable and reliable trade relations.”

This means that China intends to control not just what it buys but through whom it buys it and through what infrastructure.

That’s according to neat Party authoritative interpretations of Xi’s thought, anyway. Reality, however, is somewhat messier.

In practice, China started buying up land around the world decades ago, under the “two markets, two resources” policy by Hu Yaobang. This strategy accelerated after the 2008 global food price crisis.

The approach granted Chinese state-owned companies (SOE), private agribusinesses and funds large amounts of hectares (ha) of arable land to source produce from across the world, including Brazil. However, the moves were perceived as a foreign “land grab,” and the sovereign backlash was swift. For example, in 2010 Brazil modified its 1971’s Land Acquisition by Foreign Residents Law, to tighten foreign control over Brazilian rural land, after a series of high-profile land purchases across Latin America and an attempt to lease over 1.2 million hectares in the Philippines by Chinese actors.

China also picked up quickly that land ownership is a bad vehicle for food security at scale: a visible, politically vulnerable, and physically dispersed sourcing system cannot match control of the commercial infrastructure through which all producers must pass. That system itself is what captures value from every field simultaneously.

Thus, China pivoted away from the negative diplomatic connotations of land purchases—even if the acquisitions were not necessarily vast—and focused instead on successfully inserting itself in the value chain of global agricommodities. Changing land laws in Brazil and other countries—while reasonable from a protectionist standpoint—did not change China’s intent in addressing its food security problem.

Following this, China continued to target the Brazilian agribusiness—especially it’s soy market—as a significant source of its food imports, and took concrete steps to direct major investments there.

Upstream: China buys access to Brazil through Noble Agri and Nidera

In the early 2010’s, China’s involvement in Brazil was the highest in Latin America, which received about $10 billion in FDI from China in the 2010-2013 period, in total. Chinese involvement in Brazil kept rising in 2014-2017, right after COFCO (China’s SOE food security arm) acquires controlling stakes in two companies: Noble Agri and Nidera.

In that period, COFCO spent over $3 billion acquiring and repurposing both firms.

The first phase consisted of a tiered acquisition of majority-to-total ownership of both companies, separately. First, Noble Agri, the agribusiness arm of Noble Group, a then-powerful commodity trader based in Hong Kong. Second, Nidera, another major agricommodities trader and seed developer company based in the Netherlands.

Noble and Nidera gave COFCO—that is, China—an instant foothold in the origination business of agricommodities in Brazil, where both firms had a substantial presence.

COFCO did not just acquire a balance sheet. It acquired close to a century of embedded relationships with producers, grain elevator operators, and logistics intermediaries in Argentina and Brazil. That is institutional knowledge and commercial infrastructure that cannot be built from scratch in a decade.

In other words, in a couple M&A moves, China bypassed the entire sourcing and trading business and became itself the frontline trader at farmgate, including with Brazilian soybean farmers and cooperatives, massively cutting its own operations costs, and capturing a margin that would otherwise go to intermediaries and to the farmer itself.

Furthermore, the importance of this development lies in that it gave China a foundational entryway in a business that is virtually controlled at all stages by the so-called ABCD companies: ADM, Bunge, Cargill, and (Louis) Dreyfus.

The results were immediate. By 2018, COFCO was importing as much soy as Dreyfus and more than ADM. The ABCD companies built their positions in South America over a hundred years, China did it in less than ten years.

However, in absorbing Nidera, in particular, China acquired a bit more than logistics gains. At the time of acquisition by COFCO, Nidera Seeds (the seed business within Nidera) held the intellectual property (IP) and commercialization network of one of the most profitable soybean strains in the market: the NA 5909 RG. That soybean variety is vastly disseminated across the Brazilian soybean market. Here, the second phase of the process began, which consisted of a multipronged re-acquisition and partitioning of Nidera by Chinese entities.

ChemChina, a Chinese SOE that deals in agrochemicals first acquired Syngenta, a Swiss-based pesticides and seed business company, between 2016-2017. Syngenta, subsequently, acquired Nidera Seeds from COFCO. ChemChina is part of SinoChem, a SOE holding engaged in agrochemicals, fertilizers and a petroleum industry producer for both civilian and military purposes.

Thus, through its companies, China now has increasing leverage over the Brazilian upstream soybean market not only at farmgate through origination, but also at the input level through IP, by selling to the Brazilian farmer one of the high-yield seeds the market covets.

This is the first stop where margin compression becomes real for the Brazilian farmer. The rent extraction goes on down the value chain.

Midstream: The infrastructure buyout, further margins capture, and Brazilian politics in the way of the soybean market

Last year, COFCO acquired 979 train wagons and 23 locomotives for grain transportation stemming from the Brazilian interior. The company announced it intended to move 4 MMT from “key producing regions” to COFCO’s export terminal in the Port of Santos: TECON 11. Right next door to the coveted TECON 10.

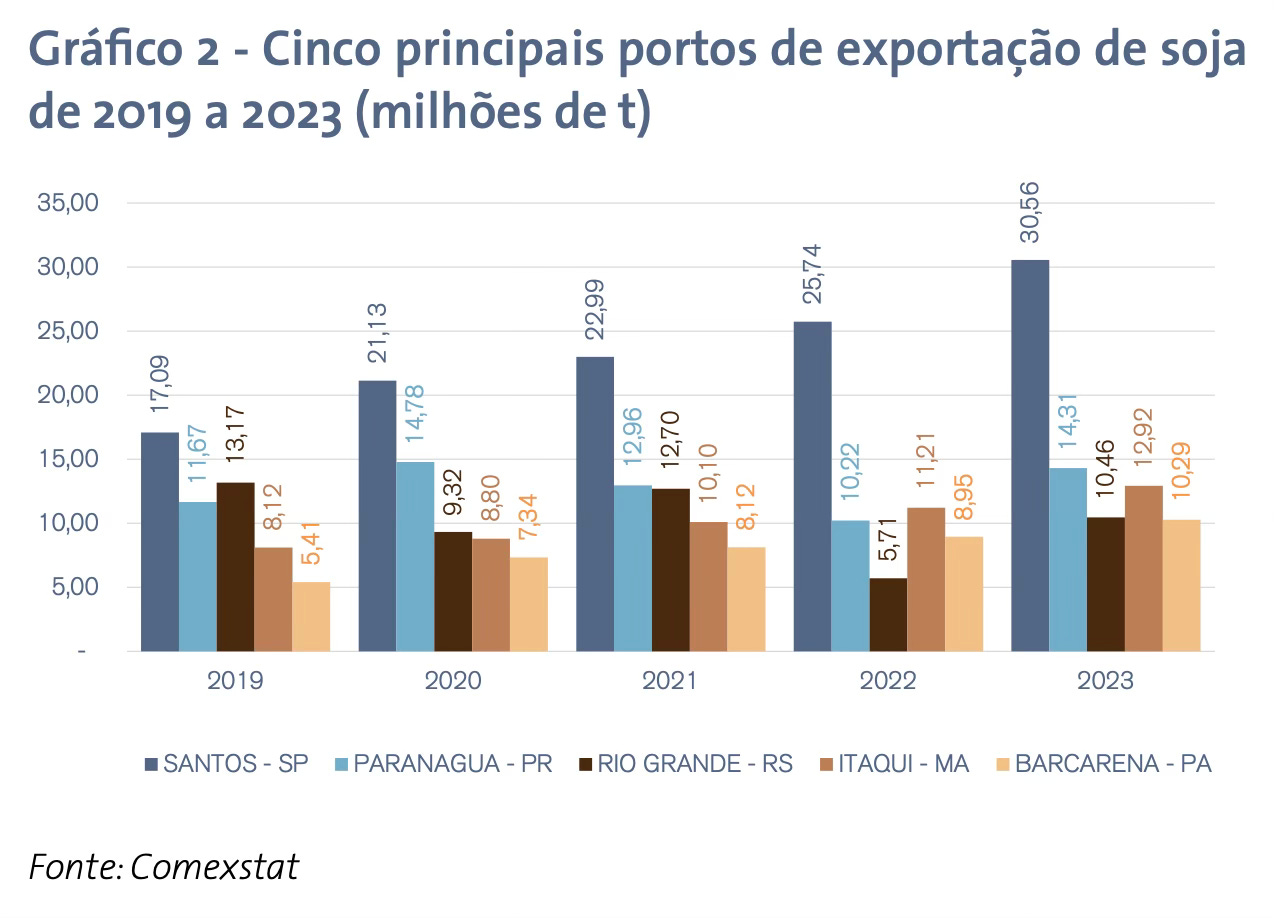

COFCO acquired TECON 11 in 2022, on a 25-year lease that granted it exclusive rights over reception, storage, handling and exporting of all cargo that reaches the terminal. The company has been working on the expansion of the terminal since. This is in addition to CMPort (another Chinese SOE) already owning 90% of the Paranaguá Port, Brazil’s second largest soybean exporting hub, after the Santos Port.

Furthermore, China, Brazil, and Peru have plans to build the so-called Bioceanic Corridor. This is a transnational logistics and transportation project that would connect the eastern Brazilian ports to the deep-water mega port of Chancay in Peru. COSCO (the Chinese shipping SOE flagship) owns 60% of the port, with little interference from the Peruvian Port Authority (APN).

While the Bioceanic Corridor remains mostly a memorandum of understanding (MOU), in practice, the idea alone is a clear signal of the true Chinese ambitions in Brazil. China aims to build a coast-to-coast trade infrastructure for the Brazilian grain market where they control the process from end to end. As a supplementary byproduct—in theory—this system would also become a closed loop, reinforcing a cycle where Brazil ships raw materials at cost and China sends back manufactured products at a premium.

China is re-defining a type of neo-colonial dependency that does not need land ownership, currency manipulation or lopsided trade and tariff agreements. Instead, the relationship is evidenced in the capture of rents at every stage of the production process: There is infrastructure control at the exit points in Santos, Paranaguá (and tentatively Chancay) of the flows control through input (seed IP) and origination (trade and infrastructure) at the interior points.

This is also where Brazilian politics come in again, and realities on the ground bite the soy industry.

Last February, the Lula administration walked back a privatization decree that put Brazil’s northern waterways in the hands of grain operators and logistics companies. These are the three rivers (Tapajós, Tocantins, and Madeira) collectively known as the backbone of the Arco Norte system, which liberates Brazil’s soybean production from the landlocked interior into the Atlantic, via the Amazon river, to which the Arco Norte is connected.

Indigenous peoples in the lower Tapajós river protested that the privatization occurred without their social licensing it, and thus they occupied Cargill’s facilities in Santarém. The Brazilian government ratified the Indigenous and Tribal Peoples Convention (ILO 169) in 2004, so it had to abide by it and side with the protesters, as it was the indigenous peoples’ right.

However, this poses a serious cost chokehold for the soybean market in the Brazilian interior. To the landlocked region, Arco Norte is the cost competitive alternative to the Santos route in the Southeast. Brazil’s center-west region, El Cerrado, has become the tropical savannah equivalent of the American Cornbelt in the Midwest, yielding the highest volume of soy in the country. The original privatization decree aimed to modernize, dredge, and build more grain capacity in the Arco Norte. If that possibility is delayed indefinitely or taken away altogether, cost competitiveness will erode for the region. Thus, the natural reaction of the Brazilian farmer in Mato Grosso or Tocantins may be to turn to China’s growing infrastructure in the Southeast, and even begin to consider the Bioceanic Corridor to Chancay as a realistic option. Political pressure will follow, and margins will compress even more for the farmer.

Again, if the infrastructure owner is also the biggest buyer (COFCO), then the rent captured at the infrastructure layer effectively reduces what the Chinese state pays for delivered grain. The Brazilian producer receives less than a competitive market would deliver.

The point is not that Brazilian producers have no options, the price at which COFCO buys from a farmer is not set in a vacuum, but at the margin of the next best buyer. The point is that the progressive concentration of infrastructure in Chinese state hands shifts the competitive equilibrium in ways that compress producer margins at the edge.

Brazilian producers are not being impoverished by China, nor would they be better off in a world with no Chinese investment, but they are not receiving the competitive market value of what they produce, given the investment Brazil made in its own agricultural development. The producer works harder, plants more, deforests more, and the margin improvement gets captured with the terminals, the trains, the ports. Also, the Brazilian state itself is a participant in this system, not merely a victim of it. They favor Chinese investment and simultaneously create policy bottlenecks (i.e. the Arco Norte walk back) that may drive the market to the Chinese.

China captures Ricardian rent by way of capturing infrastructure rent. The natural and technical advantages of Brazilian farming (abundant and fertile soil, water resources, effective agrochemistry, efficient and mechanized systems) that would go to the farmer in a competitive market gets transmitted instead to the trade and terminal side.

The result is that Brazil’s agricultural prowess is subsidizing Chinese food consumption.

Downstream: Chinese S&D control, future price-setting capacity, and the Brazilian farmer’s exposure.

As COFCO’s margins widen in its trading book, no Brazilian farmer is being cheated on any one contract. COFCO’s vertical integration through the value chain and its “sister” Chinese SOEs (and private companies) can absorb and redistribute costs, internally, in a way that the farmer is offered a price that clears the market while still capturing the rent efficiency as profit.

Eventually, if COFCO controls enough of the soy origination business, it can time its buying. It will know, better than any market participant, what real harvest volumes are, what is in storage, and what is moving at any given moment. That information advantage, combined with the ability to accelerate or slow throughput at terminals it controls, means it can influence the conditions under which prices are discovered.

This is not to say that China—today a price taker—may come to set prices itself, only that they may influence the conditions of their discovery.

Vertical integration will not give China the power to dictate what Brazilian soy costs. However, it may give China the power to systematically ensure that Brazilian soy costs less to deliver to China than any competitive alternative.

The Brazilian producer, on the other hand, will remain exposed to global price discovery. China, due to its massive position in the soybean sector, may get market price minus the infrastructure efficiency advantage it has built at state-subsidized cost of capital. Over time, that advantage compounds.

Brazilian politics may be waking up to this fact, nonetheless. The question remains whether they have the capacity (and the interest) to intervene. At 179.8 MMT handled per year and expanding, the fight over the Port of Santos is one of the early indicators that Brazilian regulators are at least aware of what’s at stake. Everyone wants a piece of the port, including China. To what degree Brazilian authorities understand the problem is unclear.

In the meantime, it is the Brazilian farmer who continues to be stuck at the center of economic statecraft coming at them from all angles. The farmer, the piece without which the entire system crumbles, is also the weakest. Real profits elude the Brazilian fields and the biomes they take over through land conversion, which are getting decimated in the name of production volumes that do not get re-distributed to the true owners of the wealth it generates.

Brazil spent the 20th century trying to leave its colonial past behind—often unsuccessfully. Now, they’re facing the same problem in this century, yet again. Oligopolist practices by SOEs overseas have the capacity to take what’s sovereignly Brazil’s without so much as the threat of violence, like the old powers used to do.

[1] The port of Santos, South America’s largest port by volume, sits just east of Sao Paulo and south of Rio de Janeiro, at the intersection of the southern axis of Brazil’s agricultural production. Facing the southern Atlantic, Santos handles over 5 million shipping containers (TEU) per year. The tender the government wants to issue is for a 25-year concession worth $1.26 billion in development plans. The resulting expansion of the terminal could bump Santos to 9 million TEU per year.

What to Read Next:

See The Southern Trade on Google

Want The Southern Trade analysis at the top of your feed? You can tell Google to prioritize this source by clicking on the button below.

© 2026 Manuel Reyes, The Southern Trade Group™. All rights reserved. Content may not be reproduced without permission.